Smog over Beijing’s

Forbidden City

Source: Brian Jeffery Beggerly, Flickr

THE BUDGETARY RESPONSE to the COVID-19 crisis of the People’s Republic of China (PRC) — delayed until the end of May due to the postponement of the National People’s Congress (NPC) — sparked intense speculation about how it would deal with environmental issues and energy transitions. Following the 2008–2009 Global Financial Crisis (GFC), the central government spent a massive sum of money on infrastructure projects, which consumed extraordinary amounts of steel and concrete, leading to strong increases in emissions of greenhouse gases. The construction boom also precipitated one of the worst episodes of local air pollution, the ‘airpocalypse’ that plagued the Beijing–Tianjin–Hebei region in particular between 2011 and 2014. In contrast, the new round of stimulus had the potential to accelerate China’s transition to clean energy, if investment was targeted at renewables, electric vehicles, hydrogen, and so on.1

As it turned out, the 2020 stimulus package did not provide support for a massive new construction program, but neither did it provide support for clean energy industries. In recent years, there has been a slowing of China’s push for renewables. Investment in coal-fired power plants has continued on a large scale, and further accelerated in 2020.

On 22 September, months after the worst of the COVID-crisis had passed in China, President Xi Jinping 习近平 announced to the UN General Assembly that China would aim to have carbon emissions peak before 2030, and reduced to zero by 2060.2 This ambitious plan makes keeping global warming below 1.5 degrees a much more realistic proposition. The suggested trajectory to get to zero by 2060, however, appears to put most of the hard work on hold until after 2030.

The Initial Crisis Response: Priorities in a Time of Uncertainty

The NPC’s annual Government Work Report — roughly analogous to the State of the Union in the United States — was presented in 2020, as usual, at the opening of the Two Meetings: the NPC and the Chinese People’s Political Consultative Congress (CPPCC). For the first time since 1990, when an economic growth target was first announced, the latest Government Work Report did not set a target for gross domestic product (GDP). This means the politically weightier 6.5 percent annual average growth target from the Thirteenth Five-Year Plan period, which ended in 2020, was also abandoned.

Premier Li Keqiang 李克强, who delivered the report, explained that there was too much uncertainty about the pandemic’s effect on global economic activity and trade, making it all but impossible to set a reasonable growth target.3 But in China, growth targets are not so much forecasts as directives. The central government might therefore have worried that setting a target — for example, for 6 percent growth — would have pushed provincial officials to aim for that target with little regard for long-term financial viability or the environmental consequences.

Premier of the State Council of China Li Keqiang

Source: President of Russia, Kremlin website

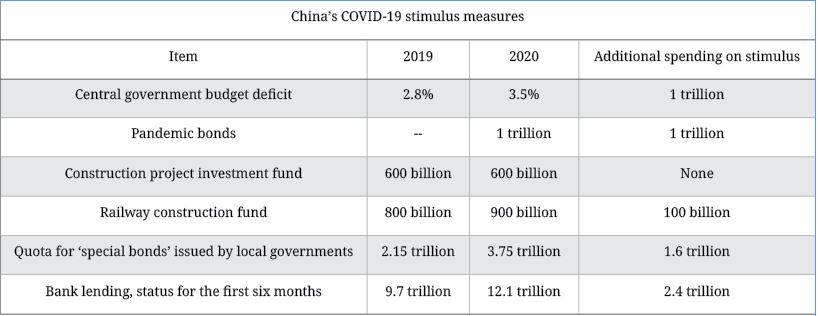

Li described the immediate priority as stabilising employment and protecting people’s livelihoods. He announced additional expenditure of 1 trillion RMB (about AU$200 billion), made available by raising the central government’s budget deficit from 2.8 percent to 3.6 percent of GDP (see Table 1). Another trillion RMB would be raised through issuance of specific pandemic bonds. Local governments were instructed to use these 2 trillion RMB to support households and small businesses through employment protection and tax relief measures.4

The budget reserved 600 billion RMB for construction projects — unchanged from 2019. The central government did increase its contribution to the national railway construction fund by 100 billion yuan, to a total of 900 billion RMB. This limited increase in railway construction will not result in great increases to emissions, and investment in high-speed rail will reduce emissions over the lifetime of the project by providing a low-carbon alternative to short-haul flights.

Support for households and small businesses cannot be said to have either positive or negative effects on the environment. Combined with spending on low-carbon transport, such support should help repair some of the economic damage caused by the pandemic without putting environmental goals at risk. So far, so good, but other elements of the recovery plan indicated that the central government prioritised the economy over the environment in the immediate crisis response.

The Government Work Report normally sets a national target for energy consumption, but that target was also omitted this year. The central government had previously committed to reducing energy intensity — the amount of energy used per unit of economic output — by 15 percent between 2015 and 2020. By the end of 2019, energy intensity had fallen by 13.2 percent.5 By causing a contraction in services and other sectors with low energy intensity, however, the pandemic will make it hard to achieve the 15 percent target. The Government Work Report also neglected to set numeric targets for emissions of sulphur and nitrous oxides and other pollutants, asking only that they be reduced, whereas in 2019, for example, it called for them to fall by 3 percent.

Table 1: China’s COVID-19 stimulus measures 6

Note: All values in RMB; 1 RMB was equivalent to AU$0.20 at the time of writing

Although the stimulus budget does not earmark central government funds for large-scale construction, it gives lower-level governments more scope to spend, and there are indications that provincial governments may do so with little regard for the environmental consequences. Local governments in 2020 were permitted to issue an additional 1.6 trillion RMB in ‘special bonds’ 地方政府专项债券 compared with 2019 (see Table 1). These bonds must be repaid from the projects they finance, rather than general government budgets. They primarily fund infrastructure projects such as roads and railways, water conservation projects, and industrial parks, where tolls or other usage fees can go towards repayment.7 The central government has also eased the conditions for lending by financial institutions, generating a 2.4 trillion RMB boost to loans in the first six months of the year.8 Following the GFC, about half of such loans were used to finance infrastructure projects.9 Assuming the same share of increases in loans this year will be used similarly, combined with the money raised by the special bonds, this would mean that 2.8 trillion RMB will be invested in infrastructure projects. Though substantial, this is only slightly more than half the amount of investment in construction resulting from the GFC stimulus.10

The State Council has, however, made it clear that it does not wish the stimulus to go towards ‘traditional’ infrastructure such as highways, bridges, and airports — projects that use large amounts of steel and concrete and support high-carbon modes of transport. In a meeting on 4 March, the Politburo Standing Committee, the highest leadership body of the Chinese Communist Party (CCP), stated that ‘new infrastructure construction’ 新型基础设施建设 was the preferred way of promoting economic growth following the pandemic.11 The very brief statement ‘to accelerate the construction of new infrastructure such as 5G networks and data centres’ immediately buoyed the stocks of relevant companies.12

The New Infrastructure concept also covers other technologies for digital transformation, such as artificial intelligence and the Industrial Internet of Things. Such investment would result in economic growth, but with far fewer emissions for every RMB spent than from traditional stimulus spending on bridges and highways. The concept further covers low-carbon energy technologies such as high-speed rail and light rail transit, charging infrastructure for electric vehicles, and ultra-high-voltage (UHV) transmission lines to transfer renewable energy to China’s coastal provinces, which would reduce emissions with every RMB spent.13

High-speed rail

Source: PxHere

Yet the central government did not specify that provincial and local governments had to spend their stimulus funds on these sorts of projects, unlike in the post-2008 stimulus budget, which clearly divided the funds into categories of projects for funding. One explanation may be that the central government is contributing proportionately far less this time. The post-2008 package was drawn roughly half and half from central and provincial budgets.14 The current package is nearly entirely funded by provincial and local governments (Table 1), which are likely to expect a greater say in how it’s spent.

A Chinese Green New Deal?

In other parts of the world, governments are using their recovery spending to accelerate transitions to clean energy and digital transformation. The European Union’s ‘Next Generation EU’ recovery package allocates hundreds of billions of Euros to renewables, clean hydrogen, and sustainable transport.15 Germany plans to spend more than one-third of its €130 billion stimulus package on ‘future technologies’, such as renewable energy, hydrogen, electric cars, and artificial intelligence.16 The Chinese central government, which wants to make the PRC competitive in these sectors, could have chosen to direct spending towards these industries.

The state has extended purchase tax exemptions by two years for ‘new energy vehicles’ 新能源汽车 (electric vehicles and fuel-cell vehicles), but only as part of a measure seeking to prop up vehicle demand more generally.17 There are clear national-level roadmaps for expanding the charging infrastructure for electric vehicles,18 with 90 billion RMB budgeted towards charging piles from 2020 to 2025.19 The stimulus measures did not add to these investments, however, nor did the government decide to spend the six-year investment budget over the next two years, for example, in order to help with short-term economic recovery.

The European Union, Germany, Japan, South Korea, Taiwan, and several other countries have recently published national hydrogen strategies. In China, there is interest in this, but policymakers remain undecided, mostly about the best financial support measures for such a strategy. Until now, it has mostly been local governments that have promoted the use of hydrogen, with a limited number of small pilot projects. Local governments and industry are unlikely to invest more in manufacturing fuel cells, fuel-cell vehicles, and hydrogen generation and distribution infrastructure when the central government appears to be dragging its feet on a national and long-term support scheme. During the design phase of the pandemic recovery package, the national hydrogen strategy remained in the stage of discussion drafts only.20

Renewable energy options such as photovoltaics (PV) and wind power, meanwhile, did not rate a mention in the central government’s stimulus package. In 2009, the government introduced a feed-in tariff — a fee paid for each kilowatt hour of electricity that goes back into the grid — for producers of wind power and, in 2011, for producers of solar power (Figure 1). These were quite generous subsidies, especially after the cost of wind turbines and PV panels started to fall rapidly. The National Development and Reform Commission (NDRC) has since reduced the feed-in tariff rates, at increasingly regular intervals (Figure 1). As elsewhere, the goal is ‘grid parity’, meaning that wind and solar would be as cheap as, or cheaper than, coal-fired power generation.

The rapid reduction in subsidies has put financial pressure on developers of wind and PV farms, resulting in reduced growth in new wind-power plants and a rapid decline in new solar-power plants (Figure 2). Despite the disruption to construction of new solar farms because of the COVID-19 crisis and appeals from developers, the NDRC followed through with its planned annual tariff reductions at the end of May, even slashing subsidies for household-scale PV by more than half.21

Figure 1: Chinese feed-in tariffs (RMB/kWh) for wind and solar PV, and the tariff for coal-fired power

Note: The coal-fired power tariff is the weighted average of provincial-level tariffs. The tariffs for wind and PV vary because China provides more generous subsidies for areas with poorer wind or solar resources.22

Figure 2: Quarterly installations (MW) of wind (top); and PV power generation capacity in China (bottom) 23

Many provincial governments have put additional wind-power construction on ice, as wind projects connected to the grid after the end of this year will not receive national-level subsidies, even if they had previously been approved to receive them.24

The haste with which the government has reduced subsidies for wind and solar power reflects not just falling technology costs. Subsidies are paid through the Renewable Energy Development Fund 可再生能源发展基金, which is financed by a surcharge on each kilowatt hour of electricity sold. After subsidy payments exceeded the fund’s earnings from surcharges, the central government was forced to make up the shortfall. By the end of 2019, the renewable energy fund was heavily overdrawn — by some estimates, to the tune of a hefty 200–300 billion RMB.25 The new rules effectively put the financial onus on the owners of renewable energy projects, with subsidy payouts intended to make up the shortfall.26 Nervous investors are scrambling to sell renewable energy assets, fearing that subsidy payments will be delayed or never paid at all.27

Coal-Fired Power Gathering Steam

In late 2014, the central government decided it would hand the power to make decisions about the development of coal-fired power to provincial governments. This caused an immediate spike in new coal-fired power plants in 2015 (Figure 3). The NDRC introduced a ‘traffic light’ system shortly thereafter, with provinces given a red, yellow or green rating, telling them to stop, slow or continue as planned with construction of new coal-fired power plants. The central government wants to limit construction in provinces where new power plants are considered to be superfluous.

Worker holding up a piece of coal in front of a coal firing power plant in the Netherlands

Source: Adrem68, Wikimedia

The restrictions are primarily targeted at areas where existing capacity can already satisfy electricity demand, and where any new power plants will simply lead to lower levels of utilisation and therefore profitability.28 The worry is that, once new plants are built, they will have to be kept running at levels high enough to recoup the investment in them. The ‘traffic light’ system therefore aimed to prevent unnecessary emissions and the construction of new plants that would have to be closed only a few years after opening.

The COVID-19 crisis appears to have made both the central and the provincial-level governments rethink this sensible policy. Large coal-fired power projects provide a quick boost in investment and job creation, and may help counter the economic slowdown, even if they have poor long-term financial prospects and put environmental targets at risk. After the NDRC relaxed restrictions on investment in coal-fired power projects in February, local authorities approved the construction of forty-eight gigawatts of coal-fired power plants by the end of May.29 In comparison, only ten gigawatts were approved in 2019. China now has a total of ninety-eight gigawatts of coal-fired power plants under construction — similar to the entire operational capacity of those in Germany and Japan combined.30

The Path Towards Zero Carbon by 2060

China’s central government did not opt to make its 2020 stimulus package about high-carbon-emission construction projects, as it did in 2009. While that has averted a potentially massive increase in emissions, China’s stimulus investment did not amount to a Chinese Green New Deal either.

When Xi Jinping’s announced a net-zero by 2060 target at the UN General Assembly on 22 September, this came as a surprise to most observers, who had seen deteriorating policy support for renewable energy in China in recent years. The announcement included a further pledge to have carbon emissions peak before 2030. Earlier pledges, including China’s ‘Nationally Determined Contribution’ (NDC) under the Paris agreement, were to have emissions peak ‘around 2030’.

It is difficult to overstate the relevance of China joining the club of countries with such net-zero pledges. The country consumes half the world’s coal, and emits 28 per cent of global carbon emissions. Chinese energy transitions therefore strongly determine global energy transitions. Although the accumulated global net-zero pledges still fall short of an emissions trajectory compatible with limiting global warming to 1.5 degrees, China’s pledge puts the world much closer to such an outcome (Figure 4).

Figure 4: Historic and projected global carbon emissions

Note: Existing net-zero pledges (by all other countries) and the Chinese net-zero pledge put the world closer to net-zero by 2050, a requirement to keep global warming ‘well below 2 degrees’. Source: IEA World Energy outlook 2020

There are, however, many different trajectories to get to net-zero by 2060. A large consortium of Chinese research institutes presented possible scenarios in October, concluding that the goal would require renewable energy production to grow about 4.5 fold by 2050, compared to today. Simultaneously, this scenario leaves most of that growth to occur after 2030, with renewables growing at a pace comparable to what has been seen in the last few years until then.

Carbon emissions, too, could keep growing slightly until just before 2030, after which they would have to come down more rapidly (Figure 5). This trajectory, and the pledge to have emissions peak before 2030, are in fact not that drastically different from business-as-usual. Chinese GDP growth is forecast to weaken, and combined with historical reductions in emission intensity of GDP, this would lead to emissions plateauing at levels only slightly above current emissions. Bringing them down from that level requires enhanced policy support.

Figure 5: Historic and projected carbon emissions for key countries

Note: China’s emission path is a suggested trajectory to net-zero by 2060 from a consortium of influential research groups led by Tsinghua university.31

The Fourteenth Five-Year Plan will guide economic and energy sector development through to 2025. This plan, which will be formally announced in early 2021, needs to lock in sustainable lower emissions development pathways if China and the world are to achieve necessary climate change goals. What Beijing sets out to do over the next five years will have far greater ramifications for climate change than its immediate response to the COVID-19 crisis.

The plan will also make clear whether Beijing will use the next five years to get a head-start on its future net-zero ambitions, or whether it will leave most of the hard work until after 2030. It is clear that the central government has committed itself to this long-term target. Now they will have to ensure that lower-level governments and state-owned enterprises follow suit. Beijing’s signalling of the new level of ambition may not be enough to prevent much of the current spending planned in fossil fuel infrastructure.

Beijing will use the Fourteenth Five-Year Plan period to get a head-start on its future net-zero ambitions

Source: Wikimedia

A Fourteenth Five-Year Plan with strong renewable energy ambitions will do more to turn this trend. That could include a strong cap on coal-fire power installations, a nationwide roll-out of the carbon emission trading system which is currently in trial phases, power market reform to further promote the competitiveness of renewables, and strong research and development programs for less mature renewable technologies, such as concentrated solar power, energy storage, and using hydrogen in industrial processes for making steel or fertiliser. Any carbon emissions prevented now will do more to mitigate global warming than the same amount of emission reductions in ten years from now.

The world is a step closer to limiting global warming with China’s pledge to reduce emissions to net-zero by 2060. In order to truly contribute to climate change mitigation, these long-term targets should be backed up with measures to reduce emissions now.